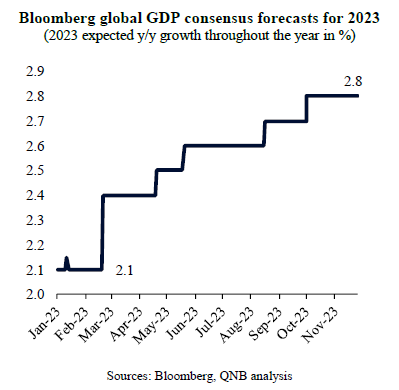

The year of 2023 started on a negative note for the global economy. Market sentiment was downbeat as investors faced sharp drawdowns in both equities and bonds. This reflected the “stagflationary” shock that took hold in 2022, when much lower than expected growth was coupled with much higher than expected inflation. In fact, at the beginning of the year, Bloomberg consensus forecasts pointed to a tepid global growth of 2.1% in 2023, significantly below the long-term average of 3.4% and the 2.5% mark that commonly defines a “global recession.”

However, global conditions proved more resilient than anticipated throughout the year. As a result, a recession indeed did not materialize, despite continuous monetary tightening, the US banking woes and industrial weakness across continents. Instead, growth expectations were consistently upgraded.

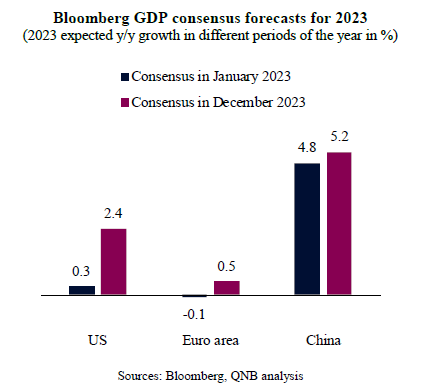

The estimated global growth of close to 3% for 2023 is a significant achievement, particularly given the initial growth expectation of 2.1%. Importantly, the better than expected performance was broad-based, affecting all major economies, including the US, the Euro area and China.

In this article, we dive into three key drivers of 2023 that caused such upward revisions in global growth expectations.

First, US growth proved to be significantly more robust than previously anticipated. With growth estimated to close at 2.4% for the year, the US economy has even re-accelerated from last year, when it ran close to its long-term trend at 2%. This took place despite the continuation of aggressive monetary policy tightening by the US Federal Reserve (Fed) throughout most of the year, which led the policy rate to the current 5.5% level. Robust consumption, in particular, which represents around 70% of the country’s GDP, helped to explain the US economic performance. US households are still benefiting from strong balance sheets, high levels of financials savings available for spending, and healthy income growth. As most US households re-financed their obligations at record low interest rates during the immediate post-pandemic period, they are mostly sheltered from the ongoing financial tightening. Therefore, consumption created a strong baseline for US GDP growth.

Second, in the Euro area, while growth sharply slowed from a strong showing in 2022, a deep recession was avoided. The energy crisis proved to be less severe than previously anticipated, due to a mild winter, more effective energy saving mechanisms, and the accumulation of high energy inventories from the previous summer. Fiscal policies remained loose to support higher subsidies and direct transfers to more vulnerable industries, households and regions. Moreover, the European Central Bank (ECB) continued with its two-pronged policy of tightening rates to fight inflation while reallocating quantitative tools to provide a backstop to highly indebted Euro area sovereigns, particularly in the southern part of the continent. This provided further financial stability, preventing the existing stagnant conditions from deteriorating into the sharper downturn that most analysts feared in the beginning of the year.

Third, after a 2022 of subdued activity and “stop-and-go” Covid prevention policies, China fully re-opened this year. China also gradually started to pivot away from restrictive fiscal and monetary policies, a tightening of the real estate sector and the regulatory clampdowns across industries. Taken together, and despite some persistent negative sentiment amongst Chinese businesses and households about the economy, these pivots provided a partial re-igniting of activity in the country, leading to moderate growth of 5.2% in 2023, above the early consensus of 4.8%.

All in all, despite a gloomy start, the year 2023 was dominated by positive macro surprises in the US, Euro area and China, which led to better than expected global growth.

Was this information helpful?