Posted on : Sun, 13 Oct 2024

Gold’s role in a portfolio has always been a topic of significant controversy. On the one hand, enthusiasts point to the importance of the precious metal as a key diversifier that also serves as a safe-haven against inflation, international conflicts and civil strife. On the other hand, detractors believe that gold is a “barbarous relic of the past,” a non-income-generating commodity with limited utility and little tangible value.

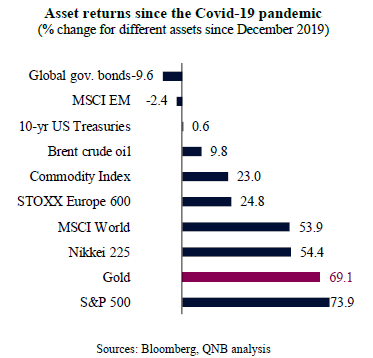

In recent years, there is no doubt that gold has been a significant enhancer to global diversified portfolios. In fact, gold reached USD 2,615 per ounce, making sequential all-time highs for months. Since the pandemic, gold has outperformed most other major asset benchmarks, including global equities, government bonds, and commodities.

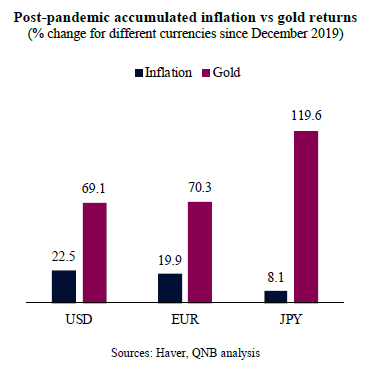

Importantly, gold has recently demonstrated its enduring value as a safeguard against inflation. In the aftermath of the Covid-19 pandemic, monetary authorities in advanced economies faced significant challenges due to a surge in inflation. This created concerns about the rapid pace of decline in the “real value of money,” as more units of currency would be needed to buy the same basket of goods and services. Not surprisingly, during this period of higher inflation, gold prices soared against most main currencies, more than offsetting the effect of consumer price increases. This offered a compelling affirmation of the long-held belief that gold is an effective hedge against inflationary pressures.

However, as disinflation gains further ground on the back of normalizing supply chains, can gold continue to perform well over the medium-term? Is the shiny yellow metal set for a correction or a period of significant underperformance?

In our view, despite a broadly normalized inflation outlook across most advanced economies, global macro conditions are still favourable for gold. Three main factors sustain our position.

First, the monetary policy cycle in the US and Europe is now a tailwind for gold prices. In recent years, cash or short-dated government securities offered high nominal yields, increasing the opportunity costs of holding gold. While nominal yields are still much higher than they were pre-pandemic in most advanced economies, this dynamic is set to change significantly over the next 24 months. The US Federal Reserve and the European Central Bank are expected to cut policy rates by 250 and 150 basis points (bps), respectively. This means that cash and short-dated government securities are going to be less attractive as investment options, favouring alternative investments such as gold.

Second, foreign exchange (FX) movements are also likely to play their part in supporting gold prices. Historically, gold prices are negatively correlated with the USD, with gold prices going up when the USD is down and vice versa. An assessment of the USD suggests that the currency is overvalued by around 9%, requiring a significant adjustment. A cheaper USD increases the purchasing power of the rest of the world for USD-priced commodities, such as gold, boosting overall demand and supporting prices.

Third, the current global economic environment is still beset with geopolitical uncertainties, such as the Russo-Ukrainian War, ongoing conflicts in the Middle East, and increasing US-China tensions in the Pacific. These factors can contribute to a heightened risk premium on traditional assets, steering investors to hedge with alternative safe haven instruments. Gold’s appeal has been further bolstered by secular or long-term trends, including the intensifying economic rivalry between West and East, a decline in international cooperation, escalating trade disputes, increasing political polarization, and the “weaponization” of economic relations via sanctions. In an era marked by more geopolitical instability, gold’s status as a tangible, jurisdictionally neutral asset that can serve as collateral in various markets becomes increasingly significant. Reflecting this movement, central banks globally have been accumulating gold at a rate unseen in generations. This supports a steady long-term institutional demand for gold.

All in all, despite the rapid global disinflation and the significant accumulated gains from gold in recent years, global conditions are still favourable for the precious metal. Gold prices are set to be further supported by easing monetary policy by major central banks, a depreciating USD and geopolitical fractures.

Download the PDF version of this weekly commentary in English or عربي

Ce contenu vous est utile ?