After decades of battling deflationary stagnation, which started after the bust of the domestic asset price bubble in the late 1980s, Japan’s macroeconomic environment has begun to change. During the deflationary period (1990-2020), the country operated in an anomalous setting of ultra-low growth, subdued inflation, and extraordinary monetary accommodation. But the confluence of the Covid-19 pandemic, global supply shocks, and aggressive fiscal and monetary stimulus appears to have finally “reflated” the Japanese economy. Post-pandemic, Japan has experienced more consistent growth alongside inflation levels that are no longer materially below those of other advanced economies. This marks a structural shift, moving Japan into a more “normal” macro regime after years of being a global outlier.

In this context, the Bank of Japan (BoJ) has initiated a long-awaited monetary policy normalization process. Negative policy rates have been abandoned, yield curve control (YCC) has been phased out, and the central bank is gradually stepping away from its role as the dominant buyer of Japanese government bonds (JGB). The policy stance has evolved in response to improving domestic fundamentals, including a tighter labour market and persistent inflation above 2%.

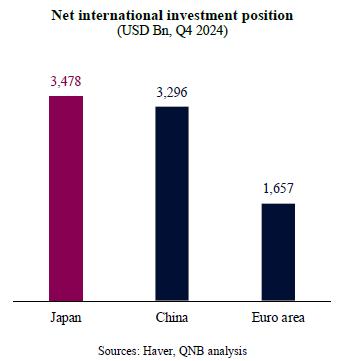

However, Japan’s normalization has raised concerns in global financial circles. Market participants fear that this policy shift could catalyze a rapid reversal of capital flows and destabilize global financial markets. These concerns are rooted in Japan’s historical role as a key source of global liquidity. Years of ultra-loose monetary policy – negative rates, YCC, and massive asset purchases – positioned the BoJ as an anchor for global interest rates. Japanese investors, in search of higher yields abroad, became significant players in global capital markets, engaging in large-scale cross-border investments and yield-seeking “carry trades.” In fact, Japanese residents hold the world’s largest net international investment position, comfortably above that of China or the Euro area.

Given this backdrop, the fear is that monetary policy normalization and rising JGB yields could trigger a capital reallocation back to Japan, tightening global liquidity and generating market stress. In our view, however, these concerns are overstated. Two main reasons explain why Japan’s monetary tightening is unlikely to generate material financial instability, either domestically or globally.

First, even after the recent adjustments, interest rate differentials against major advanced economies remain wide – both in nominal and real terms. Currently, the BoJ’s short-term policy rate stands at 0.5%, while the US Federal Reserve maintains its federal funds rate at 4.5% and the European Central Bank’s deposit facility rate is at 2%. And this comes in a context where inflation in Japan runs at 3.5%, significantly above what is seen across peers. Hence, real interest rates are still deeply negative in Japan, contrasting with positive real rates in the US and Euro area. These enduring differentials continue to incentivize Japanese investors to seek higher returns abroad, sustaining outbound capital flows and carry trade activities.

Second, the monetary tightening is expected to be orderly and well executed, preventing significant bouts of financial or economic stress. In fact, the BoJ’s normalization strategy is cautious, deliberate, and well-communicated. The pace of tightening has been slow, allowing markets to adjust smoothly. The BoJ retains flexibility and has signalled a willingness to adjust course if needed. Importantly, monetary policy in Japan remains deeply accommodative, i.e., policy rates and even the 10-year JGB yields are far below the nominal neutral rate of 2.5%. Should the gradual monetary policy tightening continue as expected, with two 25 basis points rate hikes per year, the transition to a more neutral or restrictive stance should be smoothed, reducing the likelihood of sudden capital flow reversals.

All in all, while Japan’s transition to a more conventional macroeconomic and monetary regime represents an important global shift, it is not a source of financial instability. Interest rate differentials still support global capital flows and the BoJ’s normalization is prudent and transparent. Rather than a shock to global liquidity, Japan’s monetary shift should be viewed as a positive signal of macroeconomic normalization after decades of stagnation.

Download the PDF version of this weekly commentary in

English

or

عربي