It is no secret for analysts and investors that US President Donald J. Trump has a strong policy preference to reform the current global trading and financial system. For decades, even before becoming a politician, Trump has been vocal about his negative views on large US current account deficits and the country’s net debtor position against the rest of the world, also supporting the re-shoring of manufacturing to his country.

During his first term as president (2017-2021), however, Trump did not act too aggressively to transform his policy preferences into government action. The US president was then constrained by administrative roadblocks, less political capital and experience, and more reliance on mainstream advisors that held traditional views about trade and finance.

In a more decisive break from the post-war liberal consensus on free trade, President Trump’s 2025 agenda seems to embrace his “mercantilist” or “protectionist” vision that casts global commerce as a battleground for national wealth appropriation and accumulation. At the heart of this reorientation is a very particular diagnosis that the country’s external imbalances are the result of asymmetric economic relationships, i.e., unreciprocated market access, persistent foreign subsidies, intellectual property theft, and the burdens of underwriting “global public goods,” from reserve currency provision to military security.

It is within this framework that the so-called “Liberation Day” of April 2nd should be interpreted, partially helping to explain the policy rationale of introducing a minimum baseline tariff of 10% on all US imports and additional “reciprocal” tariffs against selected trade partners, such as China. In addition, this came on top of other sectoral tariffs. While several exemptions have been already announced after the fallout of “Liberation Day” on major US asset classes, US tariffs are regardless at multiples from the norms over the last four generations.

This week, in order to better understand the challenges that Trump’s tariff policies are trying to address, we will look into the overall magnitude and size of US external imbalances. In our view, two main factors explain US vulnerabilities and help to explain why some policy groups believe it may be time to take high risks in trying to mitigate them.

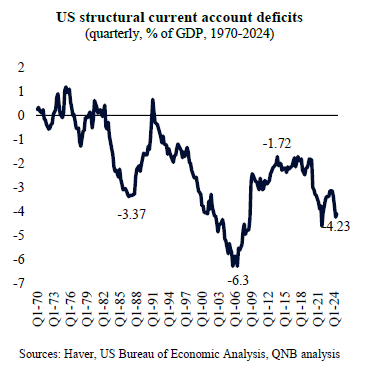

First, the US current account balance, which measures the flow of goods, services, income, and current transfers of a country with the rest of the world, presents large structural deficits. In fact, over the last 48 years, the US managed to record surpluses in only three of all those years, and none since 1991. Importantly, after a significant improvement on the current account deficits as a percentage of GDP after the Global Financial Crisis (GFC) and the Shale Revolution from 2007 to 2019, deficits have widened again after the pandemic. Nominal deficits reached USD 1.1 trillion last year and expressed a negative balance across all the main components of the current account except for services (travel, education, financial services). This means that, taken together, US households, corporates and government are consuming more than they produce, requiring external financing. The continuation of this dynamics can increase the US vulnerability to capital flows and to investment decisions from non-residents.

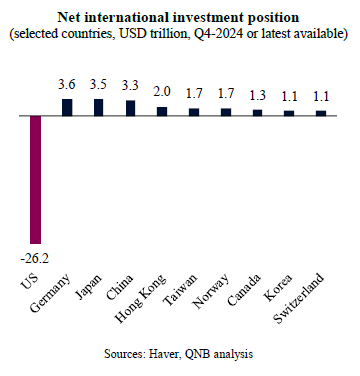

Second, the multi-decade accumulation of current account deficits has also created a significant imbalance in the net international investment position (NIIP) of the US, i.e., the balance between the assets abroad held by US residents versus assets held by non-residents in the US. In other words, the US is currently a large net debtor to the rest of the world, and particularly to successful manufacturing powers, such as Germany, Japan and China. The picture has also been deteriorating sharply, as the NIIP of the US progressed from a marginal negative figure of around 9% of GDP at the start of the GFC to 88% of GDP by the end of last year. This suggests that the US is by far the country where most global economic imbalances tend to concentrate. Over time, this level of cross-exposure could become uncomfortable to both creditors and debtors, requiring an adjustment.

All in all, there are significant US-related global economic imbalances both in terms of flows (current account deficits) and stocks (cross-asset positions). The more those imbalances grow, higher are the risks of a disorderly adjustment in the future. While Trump’s tariff policies seem to have been designed to at least partially address those issues, the ongoing and accumulated imbalances are so large that unilateral or bilateral measures are unlikely to work in terms of delivering a smooth adjustment. Just like with other major responses to large global challanges in the past, the optimum policy direction for those issues is likely to require a good level of global coordination and cooperation.

Download the PDF version of this weekly commentary in

English

or

عربي